The Financial Statements are historical documents that show the organized summaries of detailed information about the financial performance of an accounting Company for an accounting period and financial health at the end of an accounting period.

Financial Statements are the end products of the accounting process. They actually provide information about the profitability and the financial health of the business.

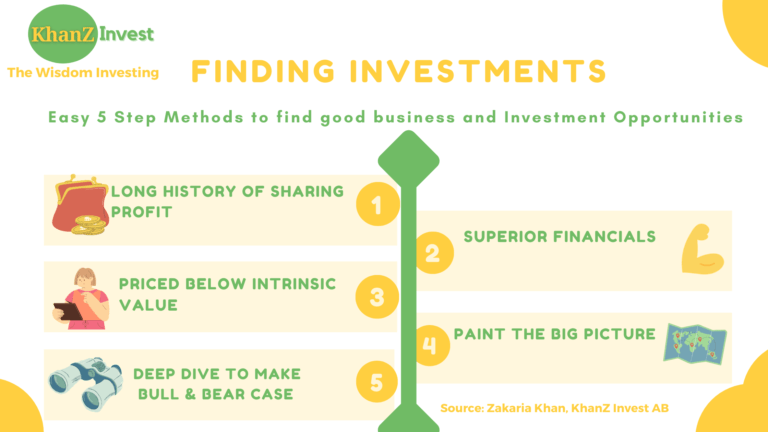

What are the major Financial Statements of a business?

A business usually prepare 3 Major Financial Statements that are as follows

- Balance Sheet is also known as a Position statement, is a statement of Assets, Liabilities and equity indicating the financial health of an enterprise for an accounting period.

- Statement of Profit & Loss also known as Income Statement is a statement of Revenue from operations, other Income and expenses during a given accounting period. It indicates the financial performance of an enterprise for an accounting period.

- Cash-Flow Statement is a historical statement indicating cash flows of n enterprises from operating, investing and financing activities and net change in cash and cash equivalent between the dates of two consecutive Balance Sheets.

The importance of Financial Statements to Equity Investors

Financial Statements are very important as it provides useful and worthy financial information of a business to various parties like Present and Potential Investors, employees, lenders and other trade creditors, customers, governments and their agencies and the public.

If you want to be an equity Investor of a business, you shall analyse and understand the financial statements of that business before buying any equity. Financial Statements tells a story about the profitability and financial soundness of the business.

Through looking into multiple years of the income statements, you will know whether the profits are increasing or decreasing. Knowing the trend of profits will help you to decide the future actions for that investment. If a company is really doing good more Prospective investors get attracted towards the company and start investing in it otherwise an enterprise will lose good investors.

Investors are interested in information on the risk and return on their investments. They need the information to determine whether they should buy, hold or sell.

Financial statements will tell you the ability of the enterprises to pay dividends. If you are investing for a safe dividend income, a low and sustainable payout ratio is very important.

Through Financial statements, you can determine the Financials health of the company. For example, if Company is borrowings a lot of money then it indicates a huge burden on Interest payment on Company so the risk of the company might increases and Investors may resist investing in that company.

Learn what is the Balance Sheet and its Importance

A Balance Sheet is a statement that provides a snapshot of the Company’s financial condition on a given date. A Company’s Balance sheet provides a lot of information that provides details about the Company’s share capital, Reserves & Surplus, Non-Current Liabilities, Current Liabilities, Non-Current Assets & Current Assets.

The balance Sheet is created based on the following simple formula

Assets=Liabilities+ Equity

Features of Balance Sheet

- It portrays the relationship between Equity, liabilities and Assets. Total of Equity and liabilities side is always equal to Assets side.

- It is not based on absolute facts rather it is influenced by accounting assumptions and personal judgments.

- It shows the financial health of the business according to the going concern concept.

Importance of Balance sheet

- The main purpose of preparing a Balance sheet is to ascertain the true financial health of the enterprises at a particular point in time.

- It helps in ascertaining the nature and cost of various assets of the business such as the amount of closing stock, amounts owned from Debtors, amount of fictitious assets etc.

- Balancesheet helps in determining the nature and amount of various liabilities of the business.

- It gives information about the amount of equity at the end of the accounting year.

Major Segments of a Balance sheet

The balance sheet comprises three major segments

- Equity

- Liabilities

- Assets

Equity

It represents ownership of the assets. Equity is also known as share capital that a company has received by issuing equity shares in the capital market. Shares are the small denominations in which the entire share capital of the company is divided into units.

Shares are of two types

- Common share

- Preference shares

If you subtract liabilities from Assets, you will get Equity, Formula as below

Equity = Assets – Liabilities

Liabilities

Liabilities refers to the amount which a company owes to outsiders for example creditors, Bank loans, outstanding expenses etc. As per the Accounting equation

Liabilities = Assets – Equity

Liabilities are mainly two types

- Noncurrent Liabilities: Non-Current Liabilities refers to those liabilities which fall due for payment in a relatively long period (normally more than a year). Debentures, Bank Loan are usual examples of noncurrent liabilities

- Current Liabilities: Current Liabilities shall have any of the following criteria

- It is expected to be settled within the company’s normal operating cycle. An operating cycle is the time gap between the acquisition of an asset for processing and its realization in cash or cash equivalent. In the absence of given information, 1 month is assumed as the duration of the Operating Cycle.

- It is held primarily for the purpose of being traded

- Current liability is due to be settled within twelve months after the reporting date

Bank Overdraft, Accounts Payable, Bills payable Short term loans etc are examples of current liabilities. Liabilities may further be divided into two more parts:

- External liabilities: refers to those amounts which a business Company has to pay to outsiders are known as external liabilities such as creditors, bank overdraft etc.

- Internal Liabilities: are those liabilities that a business has to pay to the proprietor or owners such as equity and accumulated profits.

Assets

Anything which is in possession or is the property of a business enterprise including the amounts due to it from others is called an asset. In other words, anything which will enable a business enterprise to get cash or a benefit in future is an asset. Features of Assets are as follows:

- Resources must be valuable.

- Assets/Resources must be owned by the business.

- Resources must be acquired at a measurable money cost.

Assets may be classified into the following categories

- Non-Current Assets– refers to those assets which are held for continued use in the business for the purpose of producing goods and services and are not meant for sale. For example Land & building, Machinery, Furniture etc.

- Current Assets– An asset shall be classified as Current assets when it satisfies any of the following criteria

- It is expected to be realized in or is intended for sale or consumption in, the company’s normal operating cycle.

- It is held primarily for the purpose of being traded

- Cash or cash equivalent (i.e. stocks/ short term bonds investments) are also Current assets

- Liquid Assets-Liquid assets are those assets that are either in the form of cash or can be quickly converted into cash, such as Cash, Bills Receivable, Short term Investments, Debtors, Accrued Income etc. In other words, if we exclude Prepaid expenses and closing stock from Current assets we get Quick Assets.

- Fictitious assets– also known as Nominal Assets. These are the assets that can never be realized in cash or no further benefit is derived from it in future from these assets. For example, the Debit balance of P&L A/c and Advertisement expenses.

- Wasting Assets-These are the assets that are exhausted or consumed over a period of time such as mines and oil wells. Their values reduce through being worked. These also include Patents and properties taken on lease for a definite period.

- Tangible Assets- are those assets that can be seen or touched or have physical existence like Plant & machinery, Furniture etc.

- Intangible Assets – Intangible assets are those assets that can’t be seen or touched or don’t have any physical existence. For example, Goodwill, Copyrights, Software etc.

Understand Income Statement and its Importance

An income statement is a financial statement that shows the company’s income and expenditures. Income Statement depicts the company’s Income position and profitability. It shows the result of business operations during an accounting year. It is divided into two segments

- Trading Account segment

- Profit & loss Account segment

Trading Account is prepared for calculating the gross profit or gross loss arising or incurred as a result of the trading activities of a business. It is basically prepared to show the results of manufacturing, buying and selling of goods.

Profit & Loss Account Trading Account only discloses the gross profit earned as a result of buying and selling whereas, in reality, a businessman has to incur a number of expenses to earn profit for example Advertisement expenses, Packing expenses etc.

Importance of Income Statement

- The income statement enables the business owners to be aware of the current income position. With accurate figures about the company, Managers can make swift and wise decisions.

- With the help of an Income statement, tracking the profitability of a company becomes very easy.

- It is mandatory to prepare as per the tax regulations rules.

Here is the example of Metal Store Ltd.

Some Important terms of Income Statement

- Revenue from Operations: It is the revenue earned from the business activities of the company. It includes both Revenues generated from Goods as well as services.

- Cost of Goods Sold (COGS): This term defines the cost of goods sold in the market. It includes Direct Expenses. The formula of calculating COGS is

COGS=Opening Stock+Net Purchases+Direct Expenses-Closing stock

- Gross Profit: It is the profit that is earned by a business from its core business activities. It is calculated by subtracting all the costs that are related to manufacturing or selling of goods & services from Revenue from Operations.

Gross Profit=Revenue from operations-COGS

- Operating Expenses: Operating Expenses are related to the main or normal activities of the business that are required to run the business are called operating expenses. For example– office and administrative expenses, salary to employees etc.

- Operating Profit: Operating profit is the profit earned through normal activities of the business. It is arrived at by deducting the operating expenses from gross profit.

Operating Profit=Gross profit+Operating Income-Operating Expenses

- Net Profit: Net profit is arrived at by deducting all expenses from the gross profit.

Net Profit= Gross profit -Indirect expenses

- EBIT (Earnings before Interest and Tax): EBIT is calculated as Revenue from operations minus all direct and indirect expenses except Interest and Tax. It is an important indicator to check a company’s profitability

- EBITDA (earnings before Interest, Tax, Depreciation and Amortization):– EBITDA is useful in calculating for appraising a project. It is calculated by adding depreciation and amortization expenses in EBIT.

Understand Cash Flow Statement & It’s importance

A cash flow statement is a statement showing inflows and outflows of cash during a particular period. In other words, it is the summary of sources and applications of cash during a particular span of time. It analyzes the reason for the change in cash between two balance sheet dates. The term ‘Cash’ here refers to the Cash and cash equivalents. A cash flow includes only those items which affect Cash, All non-cash items are excluded from Cash Flow.

Objectives of Cash Flow Statement

- To ascertain the sources of cash and cash equivalents from operating, investing and financing activities of the enterprises.

- To ascertain the applications of cash and cash equivalents under operating, investing and financing activities of the enterprises.

- To ascertain the net changes in Cash and Cash equivalents i.e. the difference between sources and applications under the main activities.

- To know the major activities which have provided cash during the year.

Importance of Cash-Flow Statement

- A Cash Flow statement provides information for planning the short term financial needs of the firm. Since it provides information regarding the sources and applications of cash during the year.

- A Cash Flow Statement prepared for the future period helps in preparing a Cash Budget. It helps in planning the investment of surplus cash in short term investments and to plan short term credit in advance for deficit periods.

- By preparing a Cash Flow Statement, the trend of cash is known and on the basis of the trend, important decisions are taken.

Major segments of Cash-Flow Statement

A Cash-flow statement is subdivided into 3 major segments based of the activities of a company. You will see the following 3 segments in every cash-flow statement:

- Operating Cash-flow / Activities

- Investing Cash-flow / Activities

- Financing Cash-flow / Activities

Operating Cash-flow / Activities

Operating Activities are the main profit-generating activities of an enterprise relating to the purchases and sale of goods and services.

Examples of Cash Inflow from Operating Activities:

- Sale of goods

- Received from Trade Debtors

- Cash Received from Trading

- Commission and Royalty

Examples of Cash Outflow in Operating Activities:

- Cash Purchases of gods

- Cash paid to creditors

- Operating expenses like salaries, wages etc

Below we show you an example of how the Cash Flow from Operating Activities is calculated:

Calculation of Cash-Flow from Operating Activities

Net Profit before Tax from Continuing Operations

(+) Depreciation and Amortization Expenses

(+)Deferred tax

(+) Provisions

(+) Interest on Long Term Borrowings

(+)/(-) Other Non-cash items

Changes in Working Capital

After all calculations, we get the Cash-Flow from operating activities. As a final step, subtract Income tax paid from it to get the Net cash flow from operating activities.

Investing Cash-flow / Activities

Investing activities include the purchase and sale of long term assets such as Machinery, Land & building, Furniture etc. not held for resale. These activities also include those investments which are not included in cash equivalents. Cash flow from investing activities discloses the expenditure incurred for resources intended to generate future income and cash flows.

Examples of Cash Flow arising from Investing activities are as follows:

- Cash receipt from the sale of any Noncurrent assets

- Cash payment to acquire fixed assets

- Cash receipt from the sale of shares, warrants or debt instruments of other enterprises

- Cash receipt of an insurance claim for the property involved in an accident

- Cash advances and loans made to the third party

- Cash receipt from repayment of loans & advances made to the third party.

Financing Cash-flow / Activities

Financing activities are those activities that result in a change in equity and borrowings of the enterprises. In other words, it includes those activities that result in changes in the size and composition of the Owner’s equity (Equity share capital and preference share capital) and Borrowing(both Short term and Long term).

Examples of cash-flow arising from Financing activities are as follows:

- Cash receipt from an issue of equity or preference shares

- Cash receipt from Long term and short term borrowings such as the issue of Bonds, Debentures, Bank loans, Bank Overdraft, CC limit etc.

- Cash payment for Buyback of equity shares

- Cash payment of Short term and long term borrowings including redemption of debentures, bonds, preferences share, loans etc.

- Cash payment of Interim Dividend and Previous year Proposed Dividend

- Cash payment of interest on a long term and short term borrowings.

Pingback: seo plan for ecommerce website

Pingback: organize service

Pingback: สล็อตวอเลท

Pingback: ตู้คอนโทรลสเเตนเลส

Pingback: 현금홀덤사이트

Pingback: บ้านมือสอง

Pingback: slaappillen kopen

Pingback: sig sauer spear

Pingback: briansclub 2023

Pingback: mossberg.com

Pingback: Locksmith Frankfort KY

Pingback: Nashville Real Estate

Pingback: รับสร้างบ้านหาดใหญ่

Pingback: pg slot

Pingback: y2mate

Pingback: บาคาร่าออนไลน์

Pingback: Boldenon Undecylenat Bestellen

Pingback: bonanza 178

Pingback: https://leonax.net/

Pingback: clenbuterol acheter

Pingback: bonanza178

Pingback: อนิเมะพากย์ไทย

Pingback: เครื่องมือก่อสร้าง

Pingback: เครื่องซักผ้าฝาบน ยี่ห้อไหนดี

Pingback: พิมพ์กล่องกระดาษแพคเกจจิ้ง

Pingback: Magic Mushrooms For Sale

Pingback: psilocybin Store uk

Pingback: magic mushrooms for sale USA

Pingback: ทะเบียนพาณิชย์

Pingback: aksara178

Pingback: magic mushrooms for sale online australia

Pingback: เครื่องซักผ้า 2 ถัง ยี่ห้อไหนดี

Pingback: นำเข้าสินค้าจากจีน

Pingback: Porcini Mushrooms

Pingback: สมัครyehyeh

Pingback: กายภาพที่บ้าน

Pingback: รับทำ SEO

Pingback: q188 คาสิโน

Pingback: w88 download

Pingback: ปั้มไลค์

Pingback: fryd

Pingback: buy fryd carts

Pingback: qiuqiu99 online

Pingback: togel online

Pingback: sudoku

Pingback: slot